Registering a Business for OnlyFans: HMRC, Tax and the 5 Traps We See in Our Creators

Most articles on OnlyFans and tax are either panicked or vague. The honest answer is shorter than you think. The moment your first pound flows through OnlyFans, you are self-employed. End of discussion. We manage over 100 creators across the UK, EU and internationally, and from daily practice we know the 5 things you actually need to sort and the 5 traps almost every new creator walks into at least once. This article is the practical orientation we give our models in their first week.

1. Am I Self-Employed? The Honest Answer

The most common question in our onboarding calls: "Is OnlyFans still a hobby at my level?" The honest answer is almost always no. HMRC does not ask what you want to call it. It looks at two things.

- Repeated activity. You post regularly, and with our accounts that means 3-5 OF posts per week plus chatting and PPV drops. That is not a one-off by any sensible definition.

- Profit motive. You intend to earn more than you spend. Just by paying OnlyFans for platform access and putting in the hours, that intent is there.

Once both are true, you are trading. The HMRC trading allowance of £1,000 per tax year is the only soft cushion. Above that, you must register for Self Assessment. Miss the deadline (5 October after the end of the tax year in which you started trading) and you risk penalties and backdated tax.

2. Sole Trader Registration: The 6 Steps That Actually Matter

Sole trader registration in the UK is done online through HMRC and takes about 20-30 minutes. The process is lighter than most people fear. Cost: free.

- Set up a Government Gateway account. On gov.uk, create a Government Gateway user ID. You will use this to file Self Assessment every year, so keep the credentials safe.

- Register for Self Assessment as self-employed. Form CWF1 online. HMRC issues a Unique Taxpayer Reference (UTR) within about 10 working days by post. No UTR, no filing.

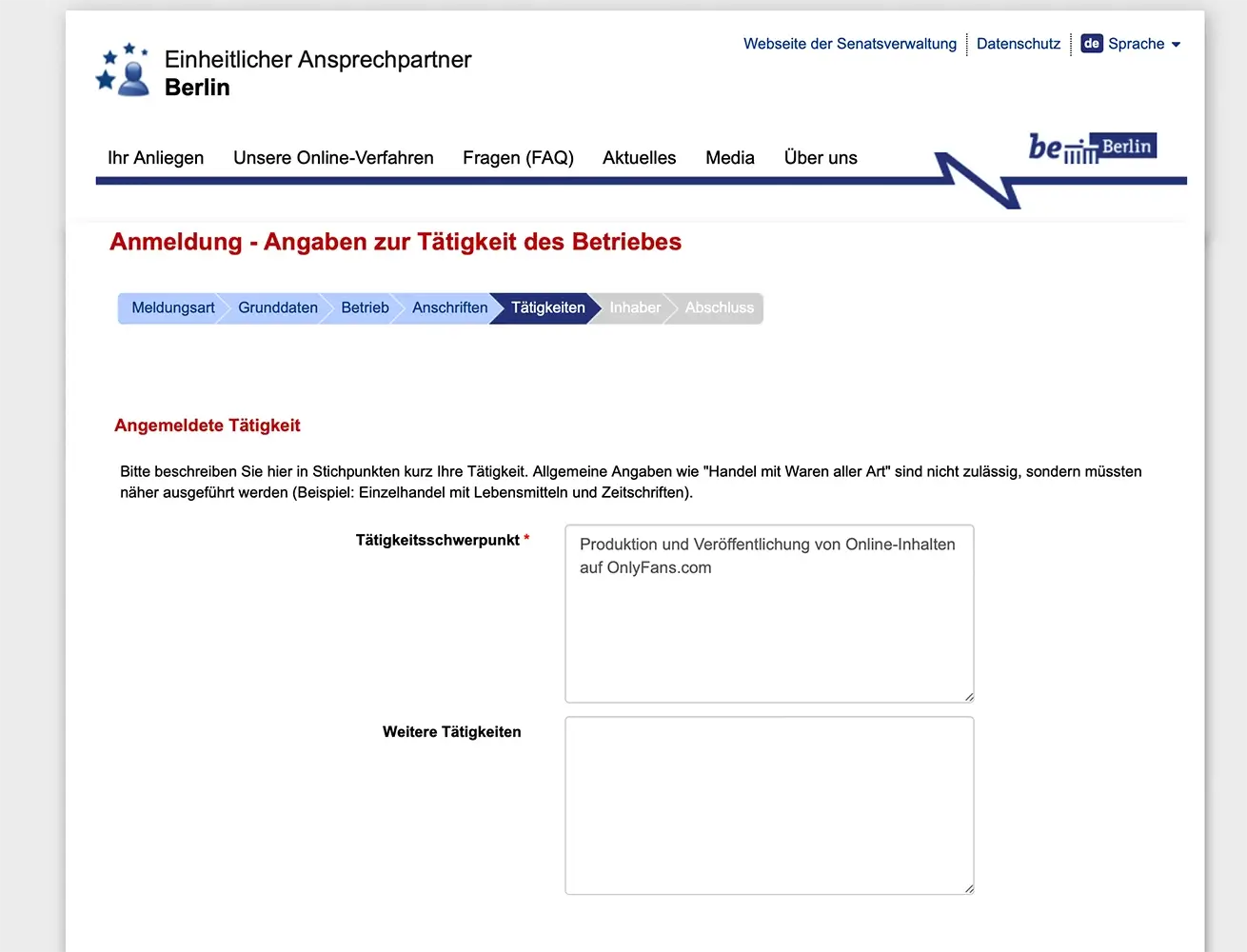

- Describe your trade clearly. A straightforward wording: "Production and publication of digital content on OnlyFans and other social media platforms." Avoid "modelling" or "influencer marketing". State what you actually do.

- Set your start date. Use the date you genuinely started trading (account creation, first post or first payout). You can register up to 5 October after the tax year in which you began without a penalty.

- Decide on structure. For roughly 95% of our creators: sole trader. A limited company makes sense later, usually once profits comfortably exceed the higher-rate threshold. More on that in section 3.

- Note the Class 2 and Class 4 NI position. National Insurance for self-employed people is collected through Self Assessment. You will see it on your tax calculation the first time you file. Don't let it surprise you.

3. Sole Trader vs Limited Company: The Structural Choice

This is the one real fork in the road early on. Sole trader means you and the business are the same legal person. Simple accounts, profits taxed through Self Assessment at your personal rate, no Companies House filings. Limited company means a separate legal entity. Profits are taxed at Corporation Tax rates (19-25%), you draw a mix of salary and dividends, and you file accounts at Companies House as well as with HMRC.

| Topic | Sole Trader | Limited Company |

|---|---|---|

| Setup cost | free | £12 at Companies House, plus accountant |

| Tax on profits | Income Tax 20/40/45% + NI | Corporation Tax 19-25%, then dividend tax |

| Liability | personal, unlimited | limited to company assets |

| Privacy | name not on a public register | director name and address publicly listed |

| Accounting burden | light, Self Assessment only | heavier, statutory accounts + CT600 |

| Typical in our portfolio | first 12-24 months | once profits clear £60-80k/year |

The rule of thumb we give our creators: stay sole trader while you are figuring out what the account is worth. Once annual profits reliably sit in the higher-rate band, run the numbers on a limited company with your accountant. For privacy-conscious creators the public director register is a meaningful downside, and tools like a registered office service are worth the small yearly fee.

4. Income Tax vs National Insurance: Two Taxes, Two Logics

A lot of creators lump these together and that is exactly when the numbers go wrong. They work on different bases.

- Income Tax. Applies to your profit (income minus allowable expenses). Every self-employed person pays it. Personal Allowance for 2024/25 is £12,570, above which the basic rate is 20%, the higher rate 40% (from £50,270) and the additional rate 45% (from £125,140). The Personal Allowance tapers to zero between £100,000 and £125,140, an effective 60% marginal band that catches plenty of top creators off guard.

- Class 2 National Insurance. Historically a flat weekly charge, but from 6 April 2024 Class 2 NI is no longer compulsory for self-employed profits above the Small Profits Threshold. You may still pay voluntarily to protect your state pension record if profits are low. Worth checking with your accountant.

- Class 4 National Insurance. The main NI charge for self-employed people. 6% on profits between £12,570 and £50,270, then 2% above. Paid through your Self Assessment alongside Income Tax.

- VAT. A separate tax on turnover, not profit. The registration threshold is £90,000 of taxable turnover on a rolling 12-month basis (as of April 2024). Below that, registration is voluntary. Above, it is mandatory.

- Payments on Account. Once your first Self Assessment shows a tax bill above £1,000, HMRC asks for two Payments on Account towards next year's liability (31 January and 31 July), each equal to half of the previous year's tax. Creators who do not plan for this get blindsided in year two by the combined bill: last year's balance plus the first payment on account.

Rule of thumb for OF creators in the first serious year: set aside 30-35% of profit for Income Tax + Class 4 NI. If you push into higher-rate territory, closer to 40-45%. VAT is separate and, when applicable, flows through you rather than out of your pocket.

5. Allowable Business Expenses: What You Can and Cannot Deduct

The best legal lever to reduce your tax bill. Allowable expenses are anything wholly and exclusively for your trade. For OnlyFans creators that is a long list. We regularly see creators missing 30-40% of their legitimate expenses in their first Self Assessment because they simply do not know what is deductible.

- Equipment. Camera, phone (business-use portion), ring light, tripod, microphone, laptop, external drives. Items used in the business can be claimed via capital allowances (Annual Investment Allowance covers up to £1 million/year for most creators, meaning full deduction in year of purchase).

- Content production. Outfits, lingerie, props and toys used exclusively for content. Everyday clothing you also wear socially: not allowable. Studio hire, location fees, travel to shoots.

- Platform and agency fees. The 20% OnlyFans fee. Agency fees (MAHO Management, for instance). Chatter services. Paid promo on Reddit, Twitter/X, TikTok.

- Software and tools. Infloww, bookkeeping software, VPN, Canva, Adobe, cloud storage. Fully allowable.

- Home office. Either the simplified flat rate (£10-26/month depending on hours worked from home) or a calculated share of rent, council tax, utilities and internet where a room is used mainly for work. Keep the method consistent year to year.

- Beauty as a business expense. A tricky area. Hair, nails, cosmetic procedures are usually not allowable because HMRC treats them as having a dual purpose. Narrow exceptions exist for clearly documented shoot-specific work. Always check with your accountant.

- Training and coaching. Industry conferences, creator coaching, photography courses. Allowable where they maintain or update skills relevant to your existing trade.

Everything needs a record. No VAT invoice or receipt in your name, no deduction. Photograph paper receipts and drop them into the bookkeeping app on the spot. That alone saves you about 20 hours in January.

6. Gross to Net: The Real Numbers We See

What actually lands in your account? A question we hear at every onboarding. The table below shows typical gross-to-net ranges for sole traders in our portfolio (single, no dependants, not yet VAT registered or treating OnlyFans revenue as zero-rated via the platform). Not marketing figures. Rough orientation. Every individual case shifts a bit, so run the real numbers with an accountant.

| Annual turnover | Profit after expenses (~70%) | Income Tax + NI (estimate) | Net for you |

|---|---|---|---|

| £30,000 | ~ £21,000 | ~ £2,200 | ~ £18,800 |

| £60,000 | ~ £42,000 | ~ £9,200 | ~ £32,800 |

| £120,000 | ~ £84,000 | ~ £26,000 | ~ £58,000 |

| £250,000 | ~ £175,000 | ~ £70,000 | ~ £105,000 |

| £500,000 | ~ £350,000 | ~ £152,000 | ~ £198,000 |

Two things stand out. First: the jump from £60k to £120k of turnover only raises your net by about 75%, because you move into the 40% bracket and lose chunks of the Personal Allowance on the way up. Second: the higher your turnover, the more your expense discipline matters. On £500k turnover with a 30% expense ratio you keep £50-60k more than someone on a 15% ratio, purely through clean bookkeeping.

7. What Goes into Your Self Assessment

Self Assessment is filed once a year, online, by 31 January for the tax year ending the previous 5 April. The return itself is where the detail work happens. The points our creators regularly trip on:

- Cash basis vs accruals. Most sole-trader creators use the cash basis (turnover counted when the money is actually received, expenses when paid). Simpler and usually fine under £150k turnover. Above that, accruals accounting is mandatory. Switching mid-stream requires an adjustment.

- Expenses claim. You can claim real expenses or, for some categories, use HMRC's simplified flat rates. Mixing methods badly is a common error. Pick an approach per category and stay consistent.

- Payments on Account. Don't forget the 31 July instalment. Half our creators in year two assume the January payment covered everything; it did not.

- UTR and Government Gateway details. Keep both safe from day one. Every year the reset-password-and-wait-for-post loop swallows at least one creator right before the deadline.

- Description of your trade. "Digital content creator" or "online media production" works better in practice than "OnlyFans creator", without misrepresenting what you do.

FAQ

When exactly do I need to register with HMRC?

By 5 October following the end of the tax year (which runs 6 April to 5 April) in which you started trading. In practice that means: as soon as you start posting with a profit motive and your income is likely to exceed the £1,000 trading allowance, register. Late registration can trigger penalties, and the longer you leave it, the messier the first return becomes.

Do I need to charge VAT on OnlyFans income?

Below the £90,000 rolling 12-month turnover threshold, no. Above, you must register for VAT within 30 days. OnlyFans generally handles VAT on fan payments at the point of sale in most territories, but the treatment of platform fees and cross-border services you buy (Infloww, US-based promo) can be intricate. This is exactly where a specialist accountant earns their fee.

What tax rate applies to OnlyFans income?

Your personal Income Tax bands. For 2024/25 the Personal Allowance is £12,570, the basic rate is 20% up to £50,270, the higher rate is 40% up to £125,140 and the additional rate is 45% above. Add 6% Class 4 NI between £12,570 and £50,270 and 2% above. Watch the 60% effective marginal rate between £100,000 and £125,140 where the Personal Allowance tapers out.

Can I claim MAHO Management fees as a business expense?

Yes. Agency fees, promotion costs and chatter services are standard allowable expenses and fully deductible. Keep the invoice, post it into your bookkeeping, done.

Should I stay sole trader or incorporate as a limited company?

Stay sole trader while profits are below roughly £60-80k per year. Simpler accounts, no public director register, no Companies House filings. Once profits consistently push into higher-rate territory, the Corporation Tax + dividend route often saves tax and adds liability protection. Run the comparison with an accountant before switching.

Do I need an accountant?

Not strictly required, but from the moment VAT, higher-rate tax and five-figure monthly revenue enter the picture, a specialist accountant at £1.5-3k per year almost always pays for themselves. Look specifically for firms that already have OnlyFans creators or adult-industry clients on their books, they know the platform mechanics and reverse-charge rules without needing the explanation.

What happens if I never register?

At worst, tax evasion. HMRC receives data from digital platforms under the OECD reporting rules (DAC7 in the EU, the UK equivalent applies from 2024 returns onwards). Unreported OnlyFans earnings show up in HMRC's data matching. The bill then arrives with back-tax, interest and penalties on top. Voluntary disclosure routes exist and are usually handled via a specialist tax adviser, but it is stress nobody needs.

Conclusion: 5 Things and You Are Properly Set Up

The perceived complexity is bigger than the real one. Creators who have these 5 points in place get through their first serious year cleanly in about 95% of cases: 1. Register with HMRC by the 5 October deadline after you start trading. 2. Pick sole trader or limited company consciously, not by default. 3. Know where you sit against the £90,000 VAT threshold and monitor the rolling figure. 4. Separate business bank account plus bookkeeping software from day one. 5. Park 30-35% of profit into a tax savings account before you spend it.

The tax side becomes a bottleneck when creators try to solve it "on the side". In practice, the opposite is faster: two hours of setup once, one meeting with an accountant who already handles OF creators, and from then on it runs. Creators who ignore it typically burn £10-30k of avoidable tax in their first serious year or get a letter from HMRC that ruins an entire quarter.